Let's say you had $2000 in credit card bills monthly and $400 in student loans and you made $2600 a month. You want to file a chapter 7. Your monthly expenses on schedule J totals $1500 so if you subtract that from monthly income it equals $1100 of DMI. So that automatically puts you in chap 13? I don't understand this. Not counting those cc bills makes it appear you have money you really don't. After me and my wife subtract schedule J from schedule I we end up with about $1500 in DMI, so does that mean chapter 7 is nearly impossible, even though without doing it we can't even afford our own place and have barely anything left at the end of the month? What are our options????

-

-

The $2,000 in credit card bills cannot be included in either the Means Test nor Schedule J. Why? For now just understand it is what it is.Originally posted by ledrums View Post

Student loans can be included in both the Means Test and Schedule J - however they cannot be wiped away in a Chapter 7.

Once you re-run the Means Test and Schedule J, it sounds like you have too much DMI on both (they are separate DMI amounts...) to qualify for a Chapter 7.

So - what do you do?

Either file for a Chapter 13 OR simply quit paying your credit card bills. If you opt to quit paying, which many on these boards have done, then start saving up for a one-time offer to pay these people off for pennies on the dollar. Most people can get settlements for between 10% and 50% of the balance owed. The trick here is to wait 6 months after you quit paying and wait for the debt to be discharged by the bank and that the debt has been sold to a collection agency (law firm). Trying to settle prior to that time is usually not worth it.

You can learn a lot about this here:

Good luck.

I AM NOT A LAWYER - THIS IS ONLY PERSONAL ADVICEOver Median Income - 10/04/10--Filed Pro Se Chap 7/ No Assets 11/10/10--341 Held 01/18/11-- No Distribution/No Funds 01/19/11--Not subject to dismissal under 521(i)(1) AND --Reaffirmation Hearing Held = APPROVED 02/10/11--Discharged

11/10/10--341 Held 01/18/11-- No Distribution/No Funds 01/19/11--Not subject to dismissal under 521(i)(1) AND --Reaffirmation Hearing Held = APPROVED 02/10/11--Discharged -

You need to assess your expenses. Are you counting everything? Not just the major items like rent/car payment but also groceries, gas, clothing, vehicle repair, household supplies, personal care needs, utilities, insurance, etc. etc. etc.

Assess your budget looking forward. If you have eaten mostly rice & beans for the past year, do not base your grocery budget on that as you won't do that without the credit card payments. I'm not saying go gourmet or eat out every night, but figure out what a normal/healthy budget should be.

If you truly have $1500 dmi left per month, then yes you'll be in a ch. 13. You can afford to repay some of your debts. But I suspect that is not your true DMI.Get mortgage modified: DONE! 7 months of back interest payments amortized, payment reduced over $200/mo

(In the 'planning' stage, to file ch. 13 if/when we have to.)Comment

-

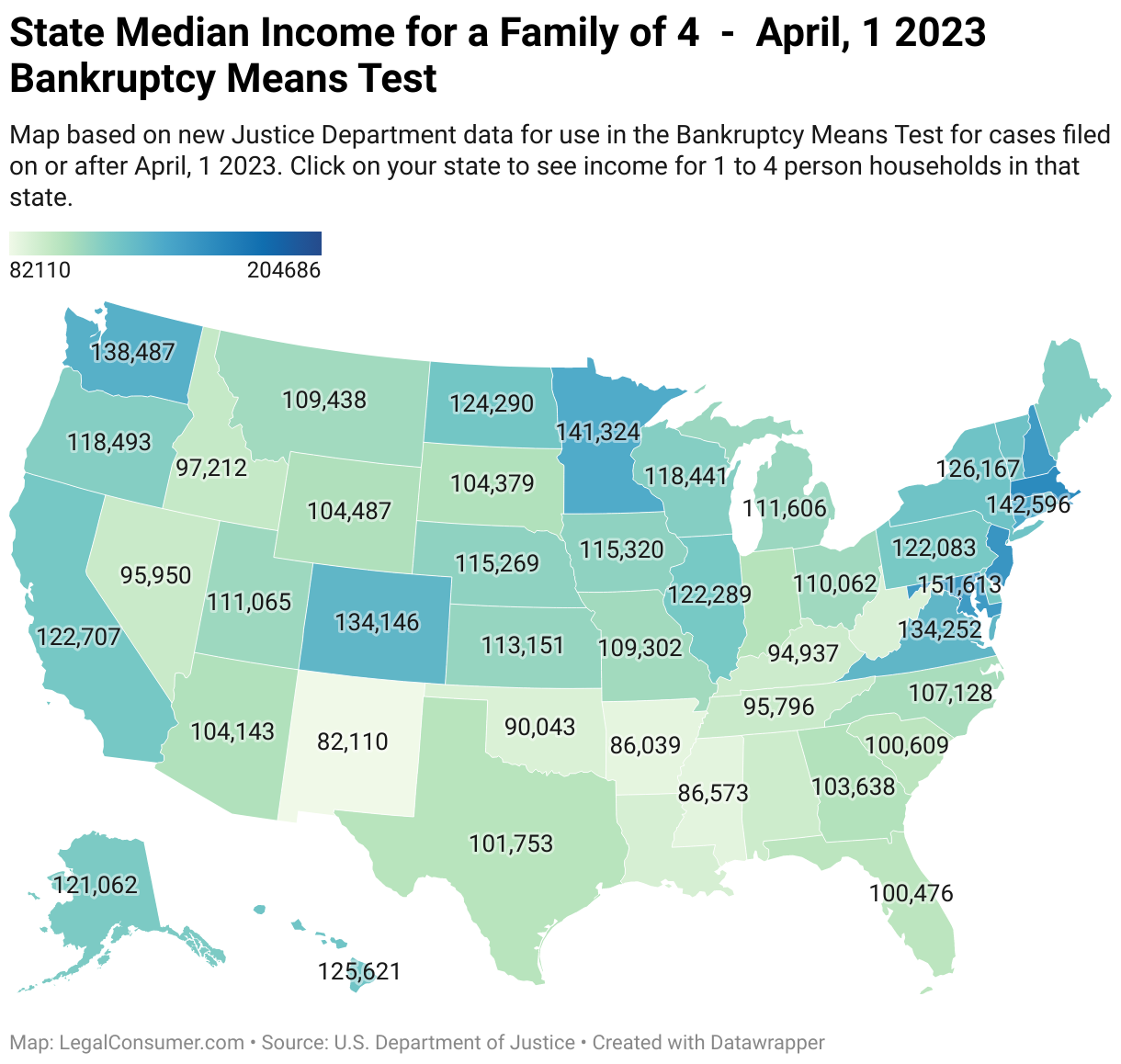

I might add that the first and main hurdle in Chapter 7 cases is the Means Test.Originally posted by SMinGA View Post

Many expenses there are set by the IRS guidelines (ex: food, clothing, rent, car payment, car operating expenses, etc.) and a debtor has little to no say so in actual expenses.

If someone cannot pass the Means Test it is very difficult to get a Chapter 7.

Fill out the Means Test FIRST and then proceed to Chapters I & J.

You can do this for free at

Best of luck!Over Median Income - 10/04/10--Filed Pro Se Chap 7/ No Assets 11/10/10--341 Held 01/18/11-- No Distribution/No Funds 01/19/11--Not subject to dismissal under 521(i)(1) AND --Reaffirmation Hearing Held = APPROVED 02/10/11--DischargedComment

Comment