Hi there all...

I've been looking into chapter 7 and found your site a few weeks ago. I've been doing a lot of reading, and still have a question about our chances at success with chapter 7. Here's the scenerio. Hubby doesn't work...hasn't since dtr born 2 years ago (this was our choice). We were fine, so we thought, and then realized we've been dipping into our cc overdraft time and time again just to make ends meet at the end of the month. Now, hubby can't get job...I'm working 40+hrs each week...two kids, one with special needs (autism), another with developmental delays. We are stressed beyond belief and know we could be okay if we didn't have all of this unsecured debt.

Chase #1 cc - $8157..0 @ 21.74%

Chase #2 cc - 9825.38 @ 29.99%

MBNA cc 15,000 @ 29.99%

House - 82,486 30 yrs fixed, 9.6% worth 85,000 (current on pay)

Walmart - 1200 (current on pay)

Medical bills - 5,000 ( 1 just went to collection)

2005 Chrysler T&C van - owe 24900 - Kelly Blue Book 18,900 (current on payments)

Attorney fees for adoption proceedings we didn't win - 2600 (pay $25 per month)

School loan (government) I know cannot be discharged - 22000

Income: 3818.00/monthly (gross) with no overtime

monthly expenses: 3154.00 (not including cc bills, or payments to other unsecured debt.)

Electric, cellphone, water & trash, heat, car insurance, van pmt, house pmt, life insurance, school loan, food, gas, personal needs, health insurance premiums, house phone, internet, cable tv, medications.

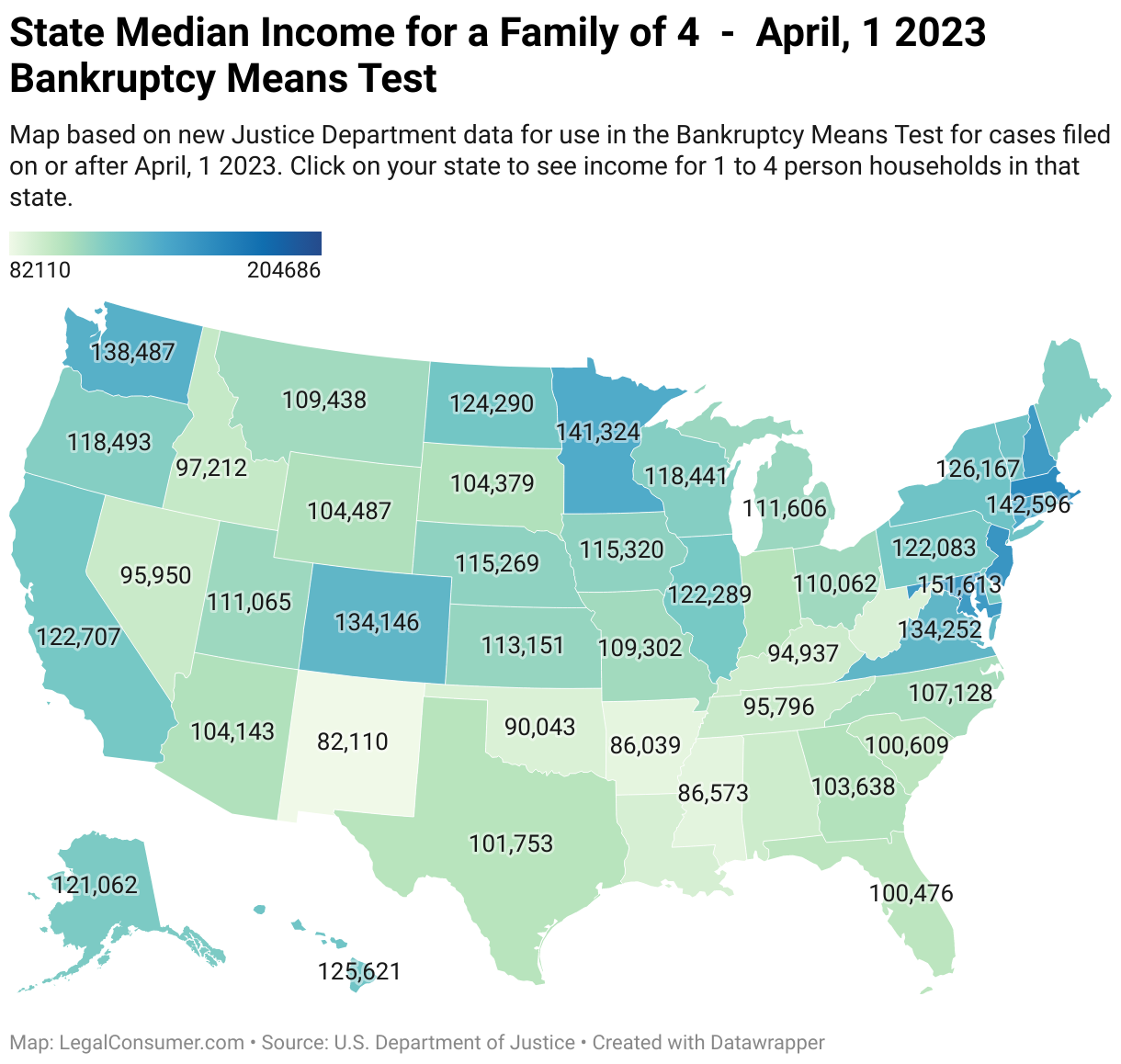

Like I said, I have been working more than my compliment at work. I work every weekend, and get full time pay for my hours at work. I can pick up shifts during the week to help supplement our income. Husband went back to school for new job training and wants to work, but we're afraid it will throw us over the median income for Indiana (66000).

Will they ask us why he is not working? He supplies our childcare when I am working...it would cost us money now for him to go to work. Once we know what direction we're headed, we can always change my hours to accomodate a job for him.

We're at our wits end, frustrated, and worried about making the right decision. Chase won't quit calling us, as we have stopped paying them as of last month. I know we'll NEVER pay down debt with those interest rates.

Any advice would be GREATLY appreciated.

Thanks in advance,

TheBrokeCouple

I've been looking into chapter 7 and found your site a few weeks ago. I've been doing a lot of reading, and still have a question about our chances at success with chapter 7. Here's the scenerio. Hubby doesn't work...hasn't since dtr born 2 years ago (this was our choice). We were fine, so we thought, and then realized we've been dipping into our cc overdraft time and time again just to make ends meet at the end of the month. Now, hubby can't get job...I'm working 40+hrs each week...two kids, one with special needs (autism), another with developmental delays. We are stressed beyond belief and know we could be okay if we didn't have all of this unsecured debt.

Chase #1 cc - $8157..0 @ 21.74%

Chase #2 cc - 9825.38 @ 29.99%

MBNA cc 15,000 @ 29.99%

House - 82,486 30 yrs fixed, 9.6% worth 85,000 (current on pay)

Walmart - 1200 (current on pay)

Medical bills - 5,000 ( 1 just went to collection)

2005 Chrysler T&C van - owe 24900 - Kelly Blue Book 18,900 (current on payments)

Attorney fees for adoption proceedings we didn't win - 2600 (pay $25 per month)

School loan (government) I know cannot be discharged - 22000

Income: 3818.00/monthly (gross) with no overtime

monthly expenses: 3154.00 (not including cc bills, or payments to other unsecured debt.)

Electric, cellphone, water & trash, heat, car insurance, van pmt, house pmt, life insurance, school loan, food, gas, personal needs, health insurance premiums, house phone, internet, cable tv, medications.

Like I said, I have been working more than my compliment at work. I work every weekend, and get full time pay for my hours at work. I can pick up shifts during the week to help supplement our income. Husband went back to school for new job training and wants to work, but we're afraid it will throw us over the median income for Indiana (66000).

Will they ask us why he is not working? He supplies our childcare when I am working...it would cost us money now for him to go to work. Once we know what direction we're headed, we can always change my hours to accomodate a job for him.

We're at our wits end, frustrated, and worried about making the right decision. Chase won't quit calling us, as we have stopped paying them as of last month. I know we'll NEVER pay down debt with those interest rates.

Any advice would be GREATLY appreciated.

Thanks in advance,

TheBrokeCouple

A NEW START!!!

A NEW START!!!

Comment