With all the debt my wife and I have, we have been contemplating bk. But I'm not thrilled at the idea of Ch 13 and would like your opinion of how close we are to Ch 7 (if that's even possible to do in this setting).

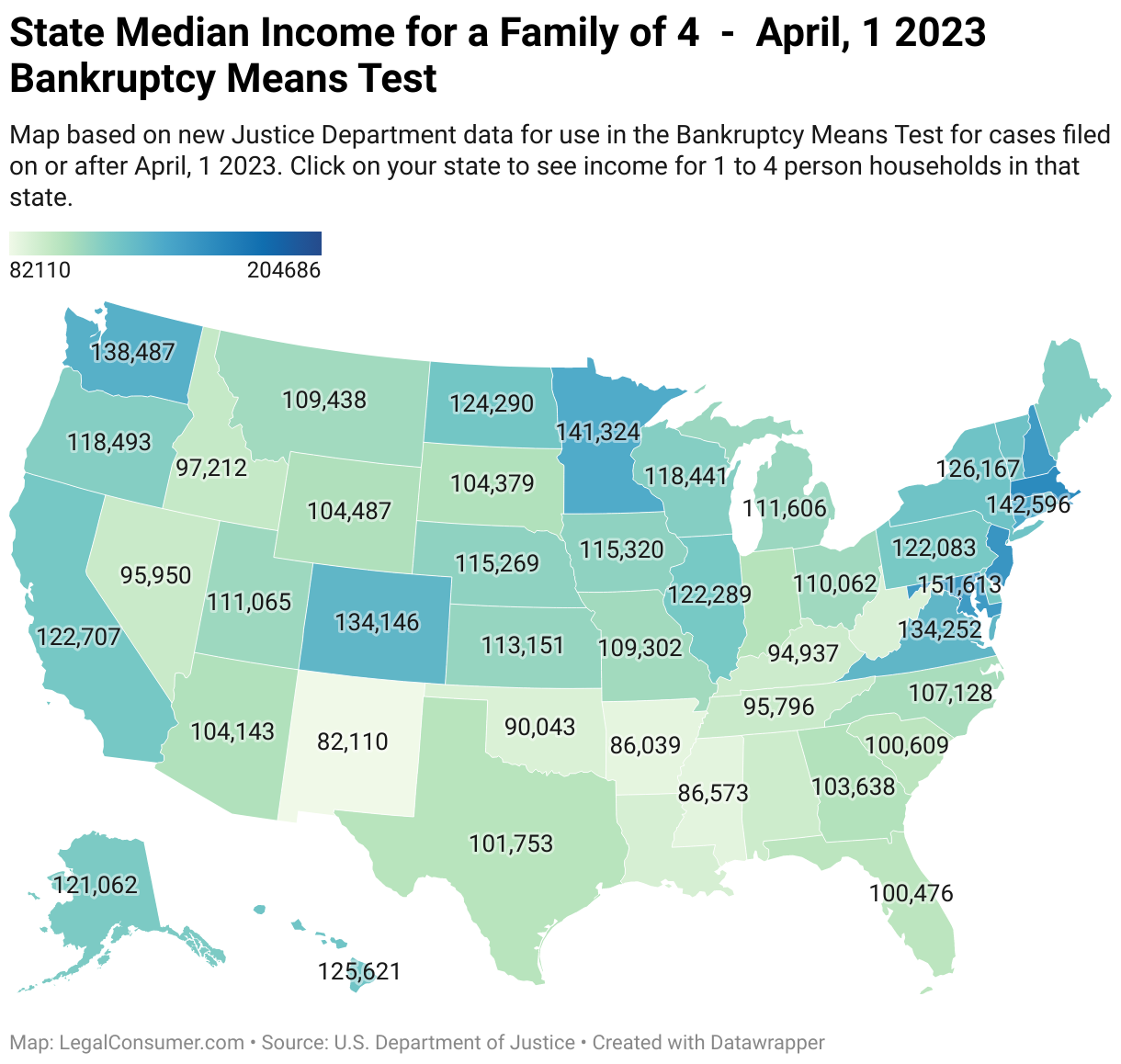

Together, we gross about $90-$95k per year, so we definitely need the means test. We live in Ohio and we are a family of 3.

-- Credit cards: ~$45,000

-- Medical bills: ~$30,000

-- Student loan debt - ~$200,000 (no, that's not a typo)

-- Wife's car - owe about $8,000 (which is approx market value)

-- My car - 2011 Kia Optima, paid off and worth about $10k, so it would likely be taken by the trustee - Ohio has $3,775 vehicle limit

-- Mortgage - We just bought a house, mortgage is $152k; not nearly enough equity for trustee to come after

-- Kay Jewlers - ~$5,000 only mention because I think this is secured debt

-- We have only a couple thousand worth of liquid cash (likely more after a tax refund)

-- About the only assets a trustee might be interested in are my guitars (but they're used value might not interest the trustee). There's also a few PCs in the house, but they're not exactly brand new. We only have one TV and I have a stereo system, which is Best Buy quality, not exactly high-end boutique components.

Mostly, the credit card bills are killing me. I can only afford to pay the minimum, which doesn't really cover all the interest and my balances have shot up over the credit limits. There is no way I can pay these down without an unknown rich uncle dies or I win the lotto.

The new house might raise some eyebrows, but we needed to move to a slightly larger house in an area where drugs were not being openly sold right across the street from us. We're trying for our second kid before it's medically too late for us (long story)... which reminds me, we have a lot of expensive fertility treatment bills coming. I've heard people can declare bk soon after buying a house, so I guess I shouldn't be too worried about it. The downpayment came from my wife liquidating her retirement account and we got a "gift" from her parents to pay off my car, otherwise the mortgage lender would not approve the loan (which is why my car is paid off).

I can't think of anything else to add and I'm not even sure you can make a reasonable estimate if Ch 7 is possible for us. I am so confused by the means test and what debt is counted, what debt is not counted. I also read something along the lines of if your disposable income over the next 60 months cannot cover 25% of your debt (unsecured debt only?) then you qualify.

So confused...

Together, we gross about $90-$95k per year, so we definitely need the means test. We live in Ohio and we are a family of 3.

-- Credit cards: ~$45,000

-- Medical bills: ~$30,000

-- Student loan debt - ~$200,000 (no, that's not a typo)

-- Wife's car - owe about $8,000 (which is approx market value)

-- My car - 2011 Kia Optima, paid off and worth about $10k, so it would likely be taken by the trustee - Ohio has $3,775 vehicle limit

-- Mortgage - We just bought a house, mortgage is $152k; not nearly enough equity for trustee to come after

-- Kay Jewlers - ~$5,000 only mention because I think this is secured debt

-- We have only a couple thousand worth of liquid cash (likely more after a tax refund)

-- About the only assets a trustee might be interested in are my guitars (but they're used value might not interest the trustee). There's also a few PCs in the house, but they're not exactly brand new. We only have one TV and I have a stereo system, which is Best Buy quality, not exactly high-end boutique components.

Mostly, the credit card bills are killing me. I can only afford to pay the minimum, which doesn't really cover all the interest and my balances have shot up over the credit limits. There is no way I can pay these down without an unknown rich uncle dies or I win the lotto.

The new house might raise some eyebrows, but we needed to move to a slightly larger house in an area where drugs were not being openly sold right across the street from us. We're trying for our second kid before it's medically too late for us (long story)... which reminds me, we have a lot of expensive fertility treatment bills coming. I've heard people can declare bk soon after buying a house, so I guess I shouldn't be too worried about it. The downpayment came from my wife liquidating her retirement account and we got a "gift" from her parents to pay off my car, otherwise the mortgage lender would not approve the loan (which is why my car is paid off).

I can't think of anything else to add and I'm not even sure you can make a reasonable estimate if Ch 7 is possible for us. I am so confused by the means test and what debt is counted, what debt is not counted. I also read something along the lines of if your disposable income over the next 60 months cannot cover 25% of your debt (unsecured debt only?) then you qualify.

So confused...

Comment