I was going to ask this on a couple of other threads, but didn't want to hijack, so I thought I would start a new one.

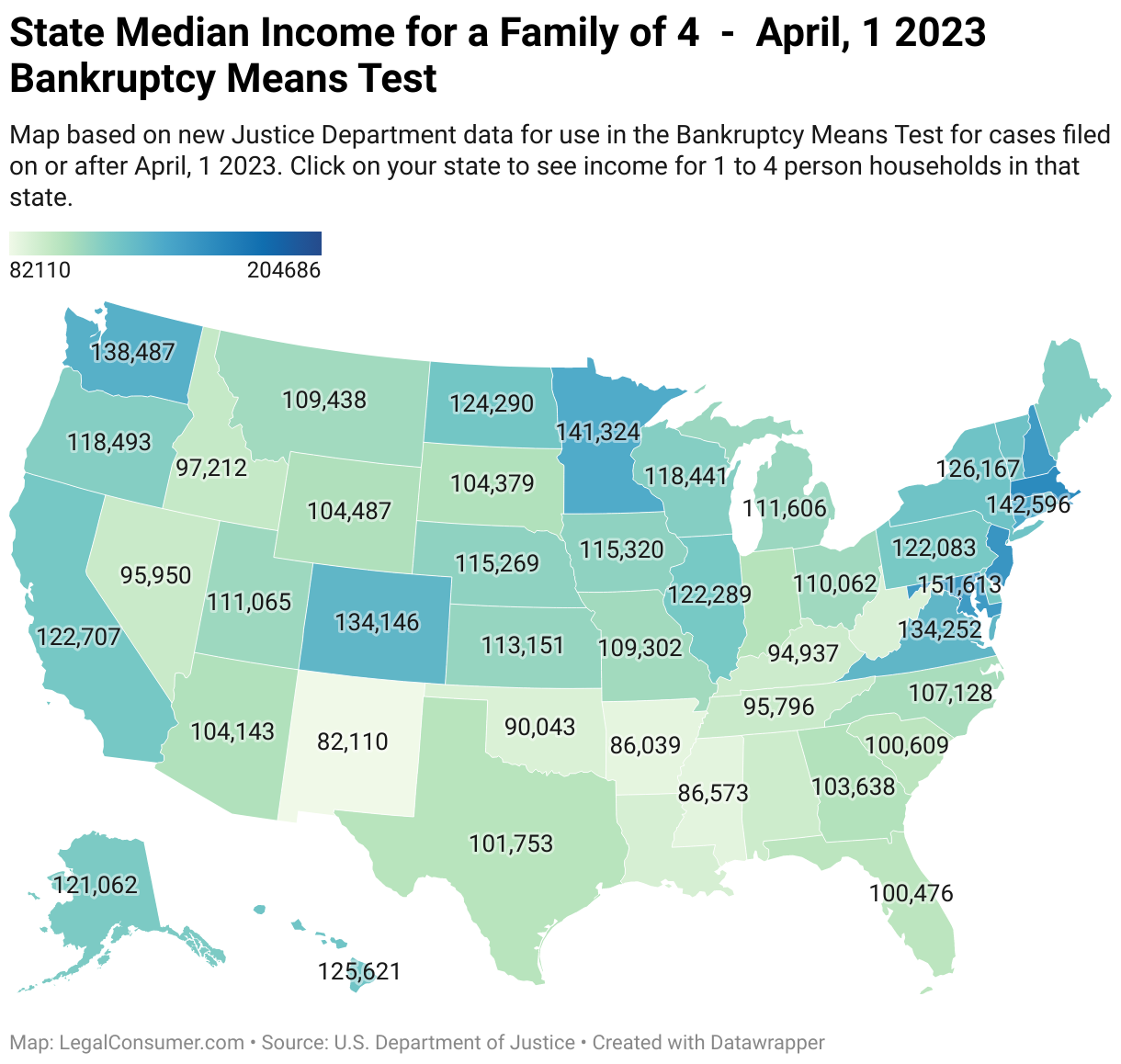

Anyway, I am preparing myself for the worst, which would be a 36 mo. chapter 13 (because, we are under median for the 7). I plugged in all of the income (incl. my SS and my children's SS) with NO exemptions other than what the IRS ones were on this website:

It said that my disposable income was $1500, or so (HA!!!!). Which, that would pay back 95K over 5 years and we are at 65K total, so I am assuming the payments would be less, but we would only be in a 3 year plan so I am sure that they could be just as high. (I don't even know if this is reliable, but I was using it as a guideline of what to possibly expect, so I don't have a heart attack in the court room)

However, I guess what I want to know is:

1. Do the trustees ever allow for the exemptions that you and your attorney put in, or do they adhere to the strict policy of only the IRS allowances? What is the norm? I'm just trying to get a feel of how strict these trustees are and if I should automatically assume that they won't allow any other exemptions or adjustments.

2. To make sure I understand the process right : You file the 13 (or convert if you are me). Within so many days (15?), you submit YOUR repayment plan to the trustee, within 30 days you begin to make payments even if the amount is not confirmed. (Are these payments YOUR proposed plan, or does the trustee make you pay what THEY decide, even without you agreeing, before the confirmation?) At the confirmation, the judge will make the official order after listening to the trustee and your attorney and you and then confirm the payment plan and time depending on his mood of the day.

3. Also, let me make sure I have this correct, The 341 is different than the confirmation right? I am assuming the 341 is first, or are they done at the same time?

(If there is a resource or sticky with the correct timeline that would be great, I couldn't find anything and I really looked!)

My last question is regarding after the plan is confirmed. Will the trustee regularly review your case to make sure that you are not experiencing a decrease in expenses or increase in pay. For example our son goes to preschool. His preschool ends in May. Will the trustee likely go after that tuition amount? How do they, if it's possible?

I know I'm posting a ton, so thanks for being patient with me! It probably seems like I am asking redundant or obvious questions. I just want to make sure I understand things completely...and also, I am having constant anxiety attacks thinking about this

Anyway, I am preparing myself for the worst, which would be a 36 mo. chapter 13 (because, we are under median for the 7). I plugged in all of the income (incl. my SS and my children's SS) with NO exemptions other than what the IRS ones were on this website:

It said that my disposable income was $1500, or so (HA!!!!). Which, that would pay back 95K over 5 years and we are at 65K total, so I am assuming the payments would be less, but we would only be in a 3 year plan so I am sure that they could be just as high. (I don't even know if this is reliable, but I was using it as a guideline of what to possibly expect, so I don't have a heart attack in the court room)

However, I guess what I want to know is:

1. Do the trustees ever allow for the exemptions that you and your attorney put in, or do they adhere to the strict policy of only the IRS allowances? What is the norm? I'm just trying to get a feel of how strict these trustees are and if I should automatically assume that they won't allow any other exemptions or adjustments.

2. To make sure I understand the process right : You file the 13 (or convert if you are me). Within so many days (15?), you submit YOUR repayment plan to the trustee, within 30 days you begin to make payments even if the amount is not confirmed. (Are these payments YOUR proposed plan, or does the trustee make you pay what THEY decide, even without you agreeing, before the confirmation?) At the confirmation, the judge will make the official order after listening to the trustee and your attorney and you and then confirm the payment plan and time depending on his mood of the day.

3. Also, let me make sure I have this correct, The 341 is different than the confirmation right? I am assuming the 341 is first, or are they done at the same time?

(If there is a resource or sticky with the correct timeline that would be great, I couldn't find anything and I really looked!)

My last question is regarding after the plan is confirmed. Will the trustee regularly review your case to make sure that you are not experiencing a decrease in expenses or increase in pay. For example our son goes to preschool. His preschool ends in May. Will the trustee likely go after that tuition amount? How do they, if it's possible?

I know I'm posting a ton, so thanks for being patient with me! It probably seems like I am asking redundant or obvious questions. I just want to make sure I understand things completely...and also, I am having constant anxiety attacks thinking about this

Comment